MLG OZ

The "goldbagger" you want.

Summary

As the gold price just hit a new all-time high, let me introduce you a well-positionned and company that could benefit from mining operations !

Market cap = AU 123 M$

Tangible Book Value = AU 145 M$

EV/EBITDA = 2,8x

EV/REVENUE = 0,34x

P/OCF = 2,1x

Revenue 5Y CAGR = 21%

It is always hard to find the stock that ticks all the boxes. Low valuation, good market conditions, margin improvements, flying under the radar, skin in the game... You have to turn an endless number of rocks until there is one. The one. Remember, in front of your screening list, you have to chose “wisely”, or you money could evaporate 10000 times faster than you think. Once you find it, you are like Indiana Jones with the Holy Grail in your hands ! You have to embrace it but still, there could be a million reasons that everything could go wrong.

Company Overview

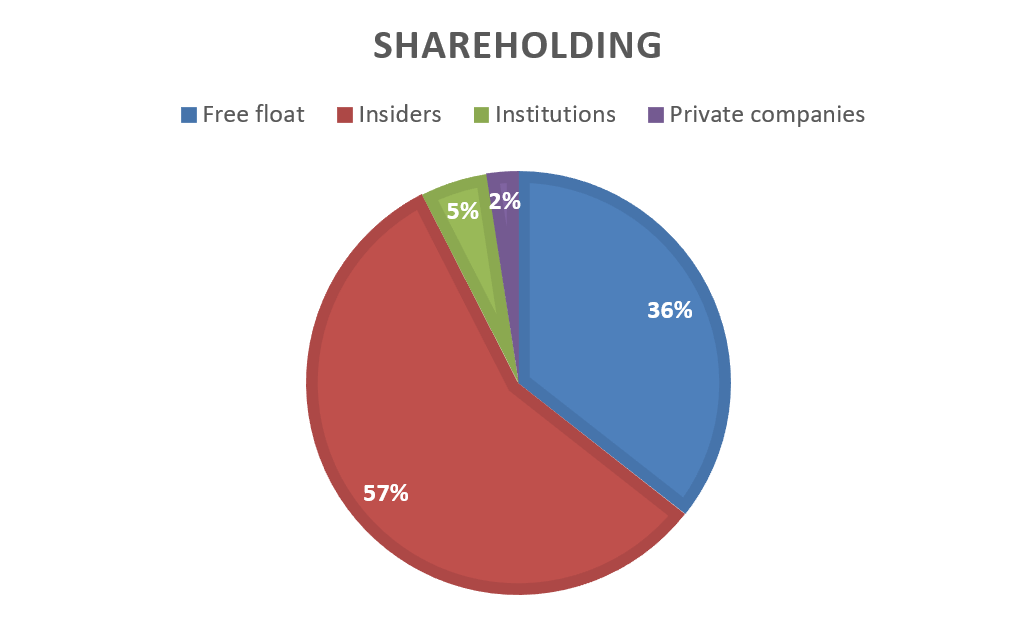

Today’s Holy Grail is MLG Oz Limited, an Australian company listed on the ASX. Founded in 2002 by Murray Leahy, its current CEO and major shareholder (owns around 50% of the shares), the company has established itself as an integrated provider of mining services and supply chain solutions. They primarily execute their activities in the gold, iron ore and base metals sectors. It operates mainly in Western Australia and the Northern Territory.

MLG Oz provides a comprehensive range of vertically integrated services that include :

Bulk Haulage and Site Services (80%)

general mine site and bulk haulage,

maintenance and management of mine site infrastructure (dust suppression and environmental management, stockpile management, and crusher feed requirements)

Crushing and Screening (8%)

ore crushing,

concrete aggregate,

road base production,

general screening services

has an extensive fleet of mobile and modular equipment capable of providing a range of crushing and screening services to multiple commodities

Civil Works and Construction (10%)

haul road construction,

TSF construction and lifts,

open pit mining services

MLG stands out with its integrated business model, combining multiple services under a single contract structure. This approach enhances efficiency and reduces costs for clients. The company emphasizes innovation, flexibility, and continuous improvement to meet the specific needs of mining projects. With over 20 years of experience and 1300 employees, MLG has built a strong reputation in the Australian mining sector, fostering long-term client relationships. They are dealing with some of the biggest names in the industry : Rio Tinto, BHP, Fortescue, Newmont etc…

Note that I don’t think MLG have a real MOAT, but it is a small actor compared to the others that play internationnally. I like this kind of company because even though they are facing competition, they often don’t act on the same playground. They have much more room to grow and more flexibility.

That’s it for the company business. Let’s move on the numbers.

Revenue, Margins and Free cash flow

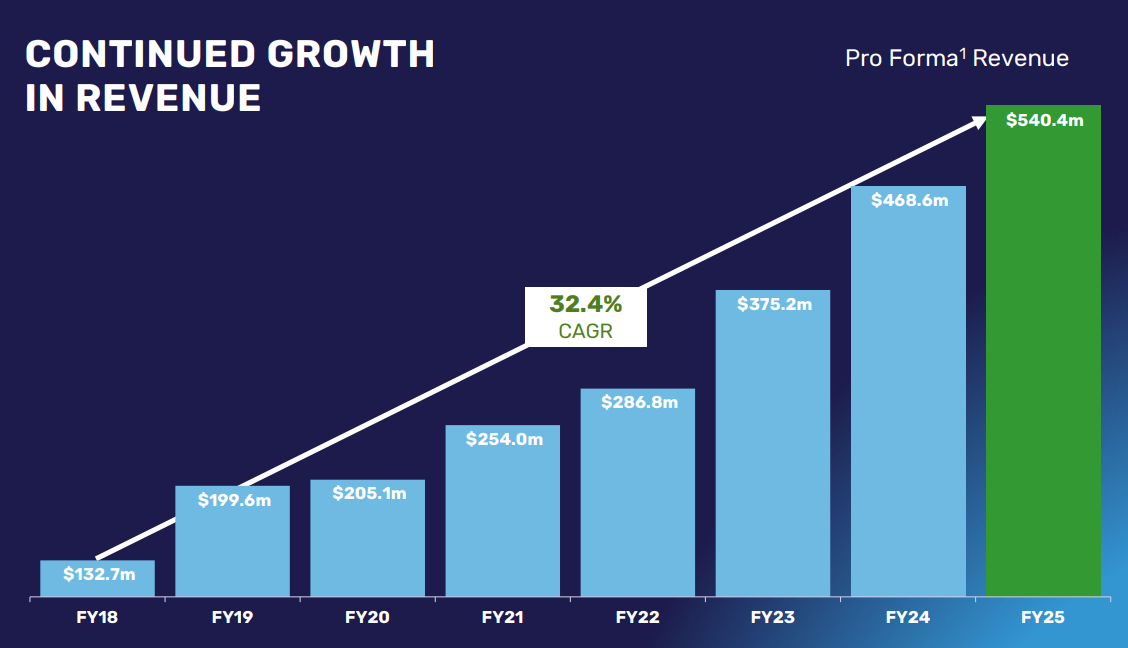

As we say in France : a picture’s worth a thousand words. Here below you can see the growth in revenue since 2018.

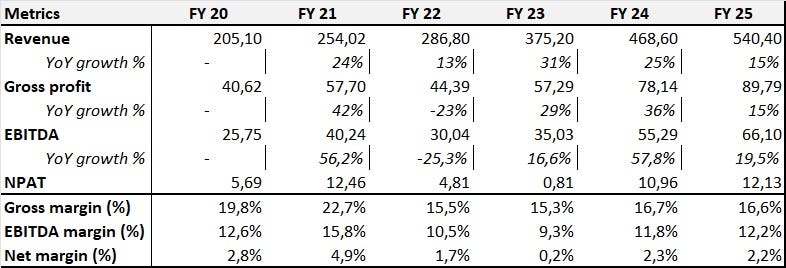

Ok the metrics starts in 2020 but it is quite enough to see :

Gross profit decreased a bit since 2020 but remains stable now

EBITDA margin dropped also but came back to almost same level as 2020

it is growing despite a stable gross profit, which shows they were able to improve their operating functionning

in fact, EBITDA margin was 13,5% in H2 vs 10,9% in H1 due to “lower activity level and [..] new capital equipment procured in anticipation of earlier contract commencement timeline”

Net margin is still low BUT we have room to grow

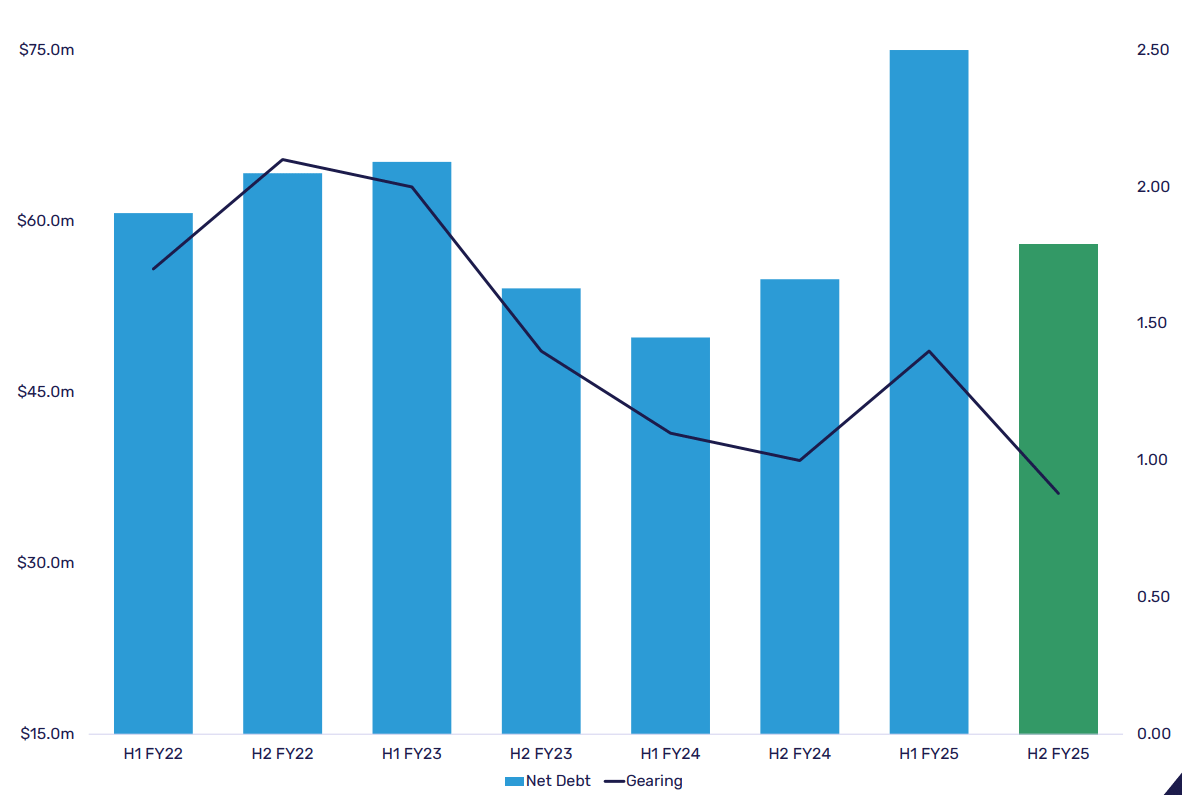

Net Debt / EBITDA stands now around 0,9x and has significantly decreased since 2022.

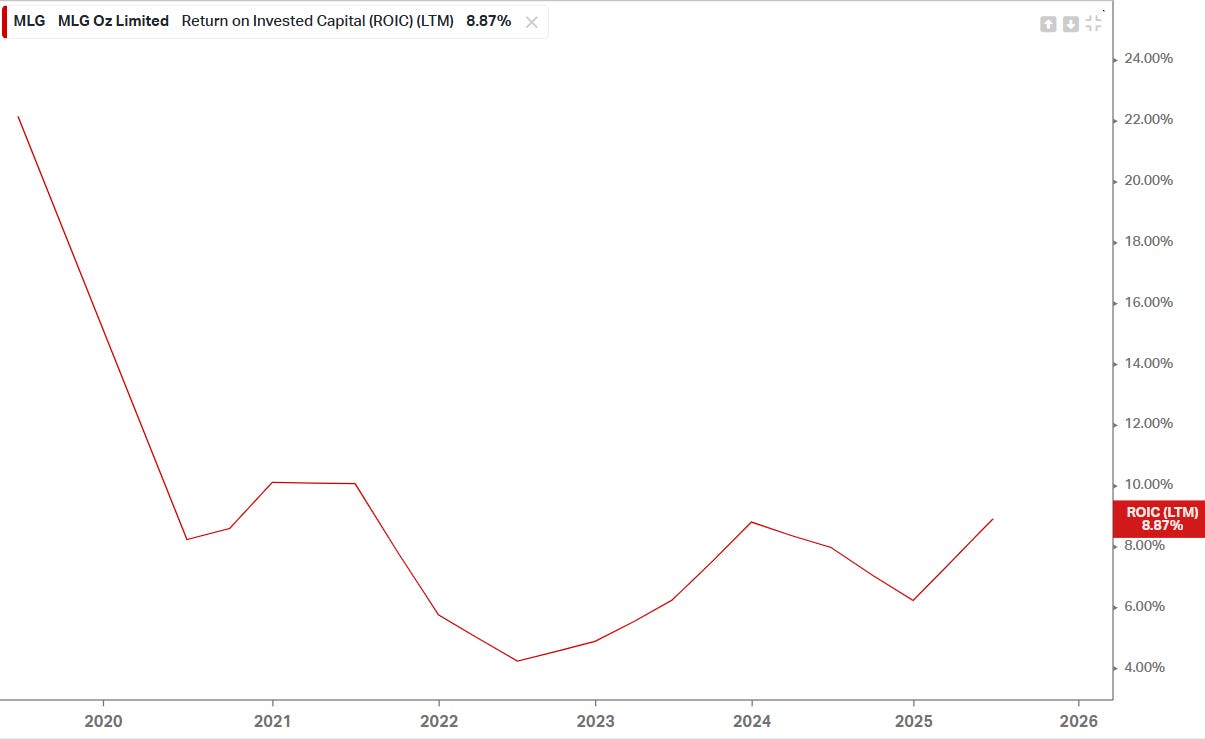

Here below you can see the ROIC evolution since 2020, which is quite correct. We can see kind of an improvement in the last 2 years, but has to be confirmed.

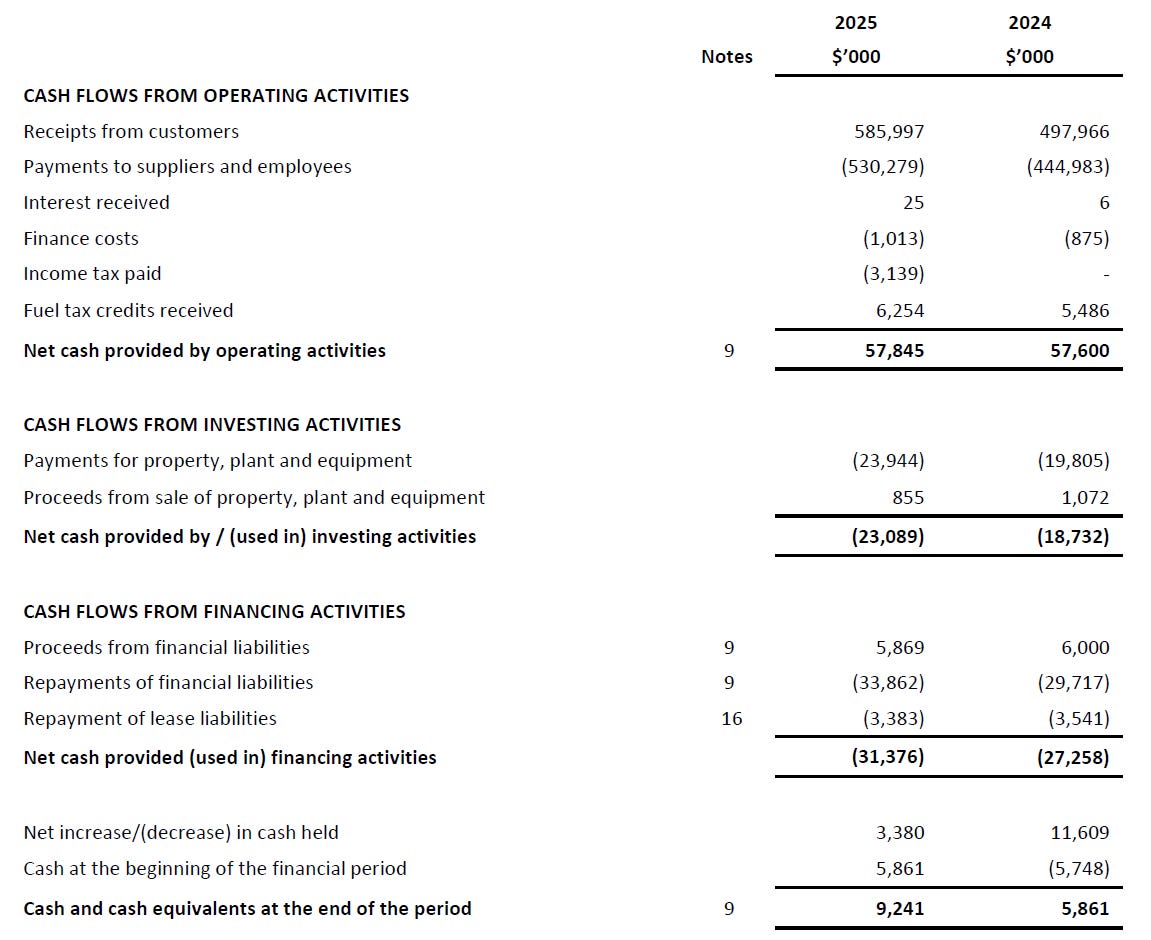

Now let’s take a look at the cash flow statement… 🧐

On the paper this company generates $34,8 MAUD free cash flow. Which leads to a 28% FCF Yield and a P/FCF around 3,5x. That is financially speaking.

The Capex is around $23,9 MAUD and is necessary to maintain the actual fleet (called “Sustaining Capex”). BUT, in order to grow they also need to lease some new equipments to achieve new contracts and so they need to spend another $33,8 MAUD (called “Growth Capex”).

Total Capex is therefore = $56,9 M AUD

In comparaison with the OpCF there is not so much left…

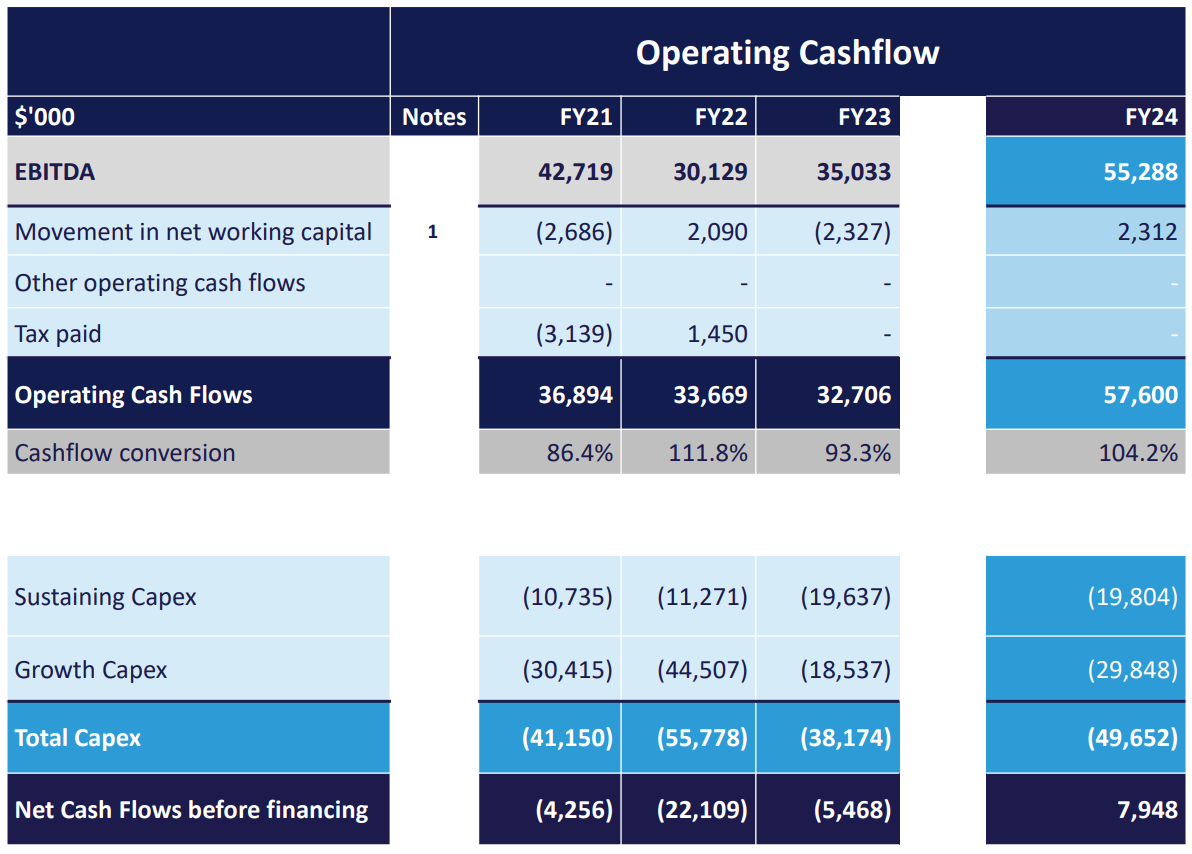

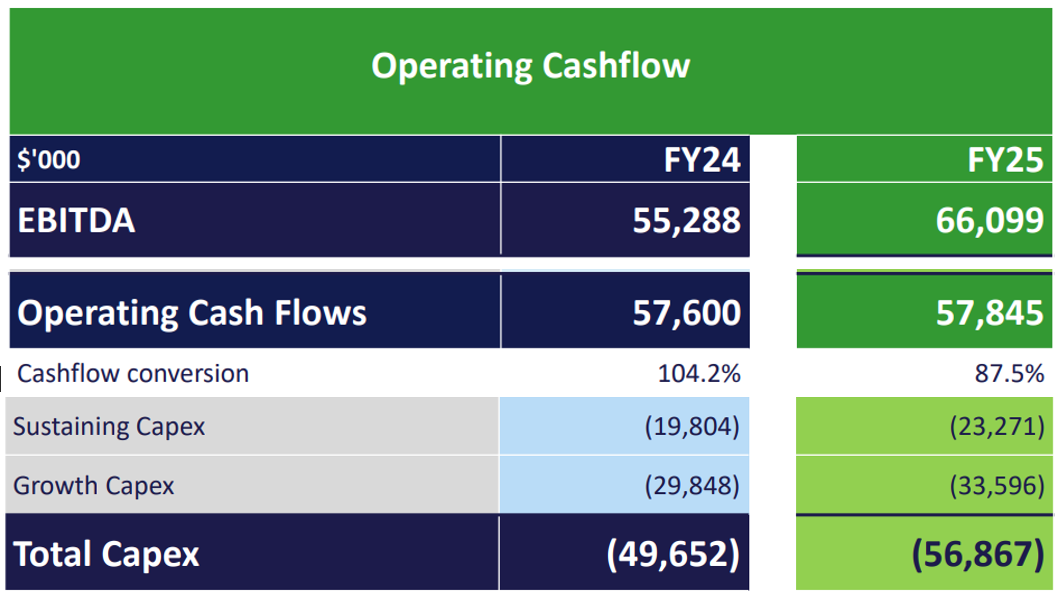

But I think that the leverage for rerating lies here. If the company is able to grow its revenue, keep an EBITDA margin at 13,5% and a stable CAPEX, they can achieve some good free cash flow generation.

We can see that Capex/Revenue was at 16 and 20% in 2021 and 2022. This ratio remained around 10% since 2023.

So let’s do some math now !

If we assume :

10% growth YoY

EBITDA margin around 13,5%

Operating cash flow conversion around 95%

Total capex around 10%

It leads us to $17mAUD of free cash flow, which represents a FCF Yield of 15% and P/FCF near 7x… not too bad, isn’t it ?

In this case I think we can at least aim a 50% rerating.

Market valuation

Here below a table I created with ChatGPT, summarizing MLG OZ valuation vs competitors.

The valuation is lower than its competitor and this is probably normal : small cap, volatile (and lower) margins, a small float etc…

BUT it trades below tangible book value and ratios are very low compared to the actual growth and compared to the momentum on gold/mining sector. I can be wrong and maybe the company won’t be able to improve margins and free cash flow, but at some point, we are talking about a profitable company in a positive environnement and a positive path.

The management is clearly focused on reducing debt level and improving magin. The story told in the reports seems to stick with the reality, the only question is, will they succeed ?

Summary

Micro Cap specialised in mining services (gold mining represents more than 90% of the activity)

CEO owns almost 50% of the company

High gold price sustains investments in mining operations

MLG OZ achieves a good level of growth but margin level is still low

Management is focused on margin improvement and reducing debt

Valuation is at its lowest, probably for good reason, but represents an asymetric opportunity

If they execute well, the FCF leverage could be really impactful and we’ll see a rerating

In this case, my target price would be around 1,0

Downside :

Price inflation directly impact their business

fuel cost

workforce shortgage (they were struggling hiring new people some time ago)

Business fully linked to gold miners investment and so gold prices

Margins are thin, volatile and lower than competitors

Hope you enjoyed this reading. It is my first one. Some information are probably missing but I didn’t want to make a very long post. I tried to summarize all the important aspects.

Of course, this is not an investment advise, you have to do your own research !

Too excited to do my first post, made some typing error. Target price is around 1,15 - 1,20 AUD if everything goes well.